Practitioner Album for Final Rule on Conformance of CAS to GAAP for Cost Accounting Standards 404, 408, 409, and 411

Summary:

On Date the CAS Board issued Final Rule (FR Ref) Conformance of Cost Accounting Standards (CAS) to Generally Accepted Accounting Principles (GAAP) for CAS 404, 408, 409 and 411.

This final rule is part of the CAS Board’s larger project to conform CAS to GAAP where comparable requirements in GAAP protect the Government’s interest and promote uniformity and consistency.

CAS 404 Capitalization of Tangible Assets

ASC 360 - Property, Plant and Equipment

ASC 360-10-05-3

ASC 360-10-20

ASC 360-10-35-4

ASC 360-10-35-33

ASC 205-Presentation of Financial Statements

ASC 205-10-20

ASC 210-Balance Sheet

ASC 210-10-45-4

ASC 210-10-S99-1

ASC 235-Notes to Financial Statements

ASC 235-10-50-1

ASC 805-Business Combinations

ASC 805-10-25-1

ASC 805-20-30-1

ASC 805-50-30-5

ASC 820-Fair Value Measurement

ASC 820-10-5

ASC 835-Interest

ASC 835-20-05-1

ASC 835-20-25-5

ASC 845-Nonmonetary Transactions

ASC 845-10-30-1

ASC 845-10-50-1

CASB Disclosure Statement Part V - Depreciation and Capitalization Practices

CAS 401 Consistency in Estimating, Accumulating, and Reporting Costs

CAS 402 Consistency in Allocating Costs Incurred for the Same Purpose

9903.201-4 CAS Contract Clauses

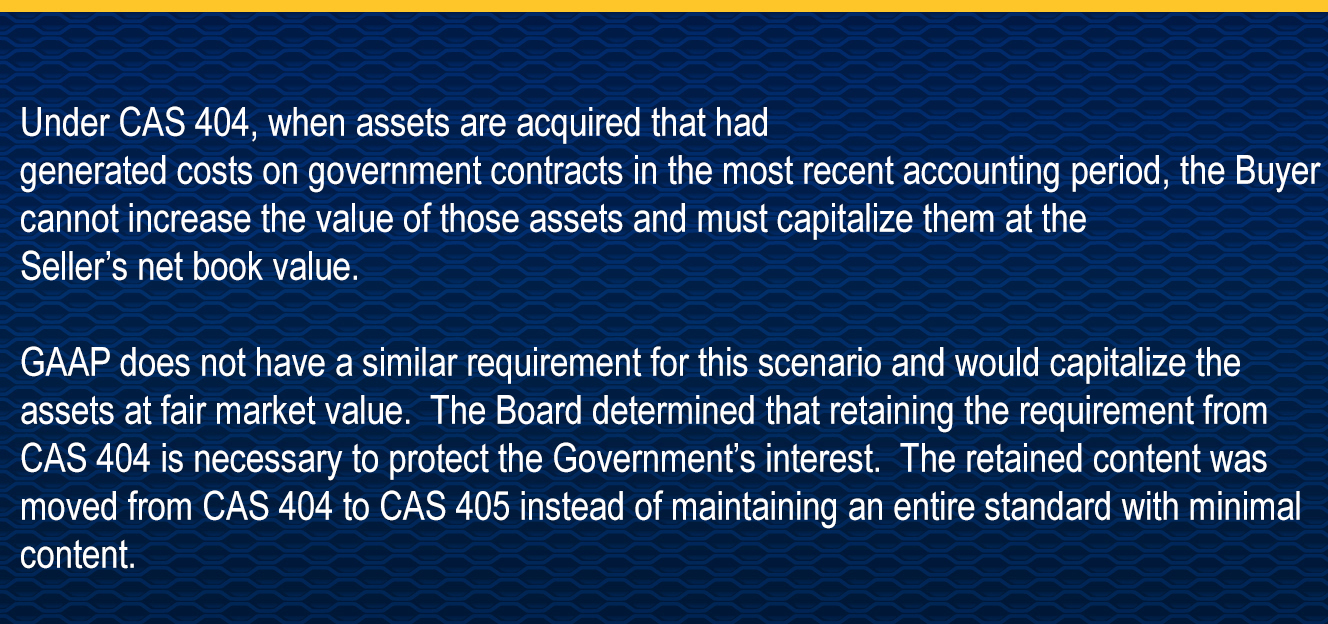

The Board determined that current GAAP requirements were essentially the same as those in CAS 404 with the exception of the requirement protecting the government from paying duplicative costs when government contractors merge or are acquired.

Retained Content

The table below identifies the content that was retained from CAS 404 where it has been relocated to in CAS 405.

Cost Accounting Practice Impacts

The Board expects that contractors will continue to follow their existing practices as they are both compliant with CAS and GAAP. Any current or future changes related to capitalization of the acquisition costs of tangible assets will be considered a voluntary change.